Depreciation Recapture and Cost Segregation

What is Depreciation Recapture?

An issue that we often encounter in our conversations with real estate investors is depreciation recapture. Recapture allows the IRS to tax a portion of the gain on the sale of property at ordinary income tax rates, rather than at the more favorable capital gains rates. This page provides a brief overview of how recapture is calculated, whether it will apply to you, and how you can work with your CPA or tax professional to minimize its impact.

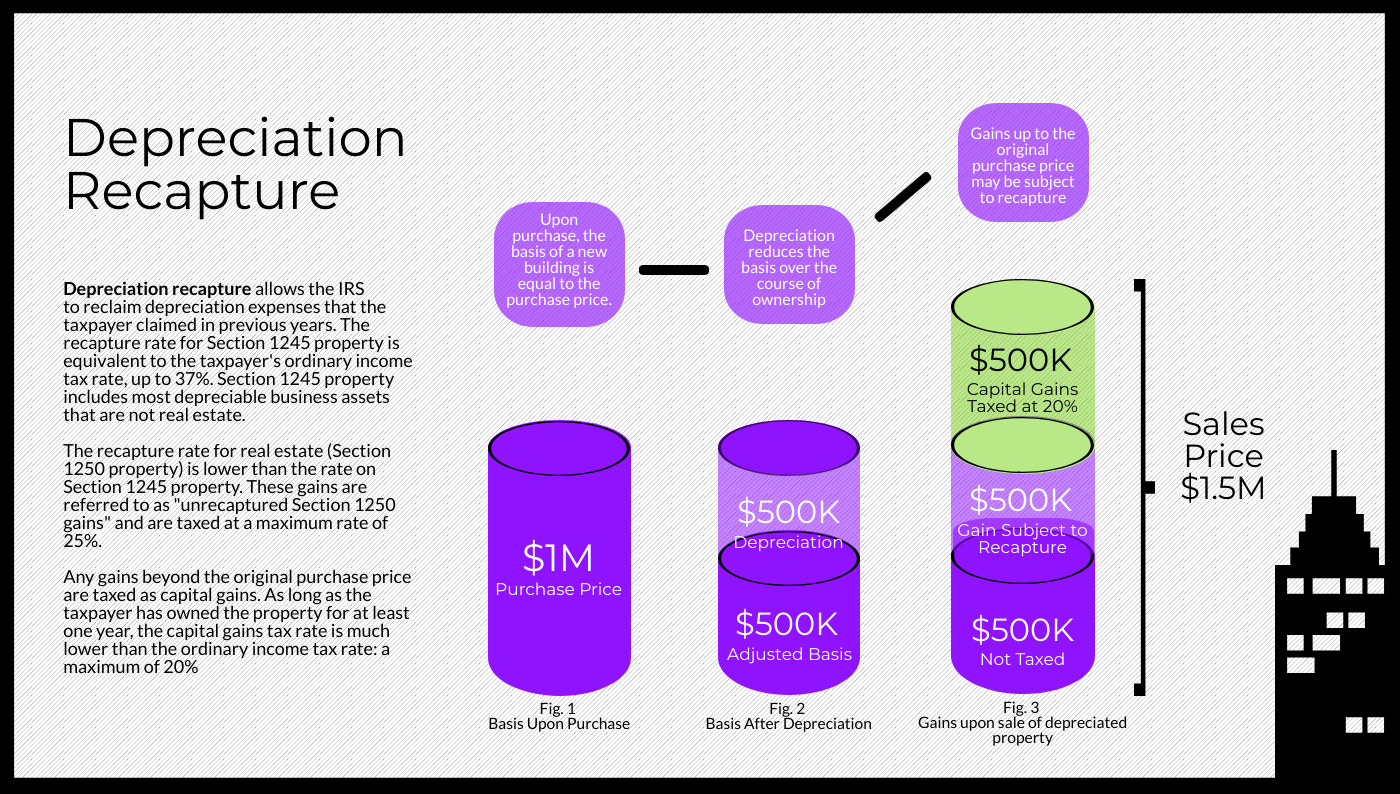

Gains above the original purchase price of an asset are taxed at capital gains rates, which are significantly lower than ordinary income tax rates. The maximum long-term capital gains rate is 20 percent, while the maximum ordinary income tax rate is 37 percent. However, any gain beyond the tax basis of an asset, but below the original purchase price, is also taxed. To calculate the tax basis, subtract the amount of depreciation claimed on an asset from the asset’s original purchase price. Consider an asset purchased for $10,000. If $2,000 of depreciation is claimed on the asset, then the tax basis is $8,000. If the asset is sold for $12,000, $2,000 of the gain will be subject to recapture and $2,000 will be subject to capital gains. In other words, any gains up to the amount of depreciation claimed are subject to depreciation recapture.

The tax rate on recaptured gains will depend on the type of property sold. When real estate is sold, gains up to the amount of depreciation claimed are taxed at a maximum rate of 25 percent. When personal property is sold, those same gains are taxed at ordinary income tax rates. Cost segregation reclassifies a portion of real estate as personal property. Thus, depreciation recapture is often a concern for property owners considering a cost segregation study.

Depreciation recapture will cause a portion of the gains from the sale of a building to be taxed at a higher rate. Click or tap the image to zoom in.

Will Depreciation Recapture Affect Me?

Depreciation recapture applies when an asset is sold. If you do not intend to sell your property, recapture should not be a major concern. If you do intend to sell your property within the next few years and you have completed a cost segregation study, a portion of your gains will likely be subject to recapture at ordinary tax rates. You should consider how recapture will affect you before moving forward with a cost segregation study.

Your CPA or tax professional’s approach to allocating the sales price of the asset when you dispose of it will have a major impact on the amount of recapture you pay. When you sell a building, your CPA will allocate a portion of the purchase price into several categories:

Building structural components (Section 1250 property)

Depreciable components that are not considered to be real property, such as 5, 7 and 15 year property (Section 1245 property)

Land

Goodwill and other intangibles

When your property is sold, you may choose to reduce the amount of gain that you allocate to Section 1245 property such as carpeting and cabinetry, and instead choose to allocate more of the gain to the structural components of the building (Section 1250 property) where you will enjoy a recapture rate of 25 percent rather than the ordinary income tax rate of 37 percent.

Any gains beyond the original purchase price of the building will be taxed at as long-term capital gains at a maximum rate of 20 percent. It’s important to note that you must hold an asset for at least 1 year in order to qualify for the lower capital gains rate. Otherwise capital gains are taxed at ordinary income tax rates.

A Closer Look: Real Property, Personal Property, Capital Gains, and Cost Segregation

Recaptured gains on Section 1245 property are taxed at ordinary income tax rates; the same gains on Section 1250 property are referred to as “unrecaptured section 1250 gains” and taxed at a maximum rate of 25 percent.

Any gains above the original purchase price are taxed as capital gains. As long as the asset has been held for ever a year, the capital gains rate is a maximum of 20 percent.

Cost segregation reclassifies some section 1250 property as section 1245 property.

When Should I Consider Cost Segregation?

Whether cost segregation will provide a benefit to you will depend on your property type, purchase date, your basis in the property, how long you intend to hold the property and your ownership structure.

If you are still wondering whether the cost of depreciation recapture will outweigh the benefits of cost segregation, we can help. We can prepare a depreciation recapture analysis that will give you a projection of how much recapture you can expect to pay if you choose to sell the building within the next five years. Our analysis can provide you with a valuable informative tool to help you can share with your advisors and empower you to make the financial decision that’s right for you. Contact us for more information, or use our online form to request a cost segregation estimate for your property.

This page is intended for general information only, and is not meant to constitute tax advice.