Unpacking the IRS Cost Segregation Audit Techniques Guide

Cost segregation studies have become steadily more popular as more taxpayers have informed themselves about the benefits of cost segregation. In response to the rising popularity of cost segregation studies, the IRS developed the Cost Segregation Audit Techniques Guide to provide guidance to tax professionals. The Audit Techniques Guide, or ATG, provides an overview of what cost segregation is, as well as guidance on what makes for a quality cost segregation study.

The ATG specifies exactly what the IRS looks for in the review and examination of cost segregation studies. This article provides a review of some of the major takeaways from the ATG. To view the guide yourself, see the IRS website.

Need a quick overview of cost segregation? Check out our “Overview of Cost Segregation” and our outline of Depreciation Methods

Cost Segregation Studies are Complex

In the introduction to the ATG, the IRS refers to the “complexity of cost segregation issues.” The complexity arises out of the fact that a cost segregation study not only identifies assets such as molding, flooring, etc., that can be reclassified, but a study also evaluates parts of the building structure (such as electrical and plumbing) and reclassifies portions of those components. This type of reclassification often requires complex determinations of electric load or water pressure. From the ATG:

“[The study] may also identify that, for example, 15 percent of a building’s electrical distribution system (EDS) directly supports § 1245 property, such as specialized kitchen equipment. Based on that conclusion, the study will then treat 15 percent of the EDS cost as § 1245 property along with the identified § 1245 branch circuits...The allocation of building components to § 1245 property is often a contentious issue.”

The issue is “contentious” because taxpayers have a strong incentive to classify as much property as possible at 1245 property because of the tax benefits of doing so. This contention came to a head in the landmark court case Hospital Corporation of America vs. IRS. This landmark case forms the basis for why and how cost segregation is allowed today.

In light of the complexity of cost segregation studies and the contentious tax issues surrounding them, engineering-based approaches to cost segregation are often considered more reliable. The ATG provides an overview of different methods of completing cost segregation studies ranging from detailed, engineering-based approaches to “rule of thumb” approaches.

The most detailed approach is the “detailed engineering approach from actual cost records.” While the ATG says that this approach is generally “…the most methodical and accurate approach,” it is not always possible to get detailed construction cost information from a building. Taxpayers often want to complete cost segregation studies on buildings that are years or even decades old. In such cases, there may not be enough documentation to support an engineering-based study “from actual cost records.”

Another engineering-based approach is the “detailed engineering cost estimate approach.” This engineering-based approach is used when detailed construction cost records are not available. While this method may not be as reliable as using actual cost records, the ATG notes that with this method, “reasonably accurate cost allocations are possible.”

According to the ATG, the IRS does not require a specific cost segregation method, although it’s reasonable to speculate that less reliable approaches (such as the “rule of thumb” approach) could be subject to more scrutiny.

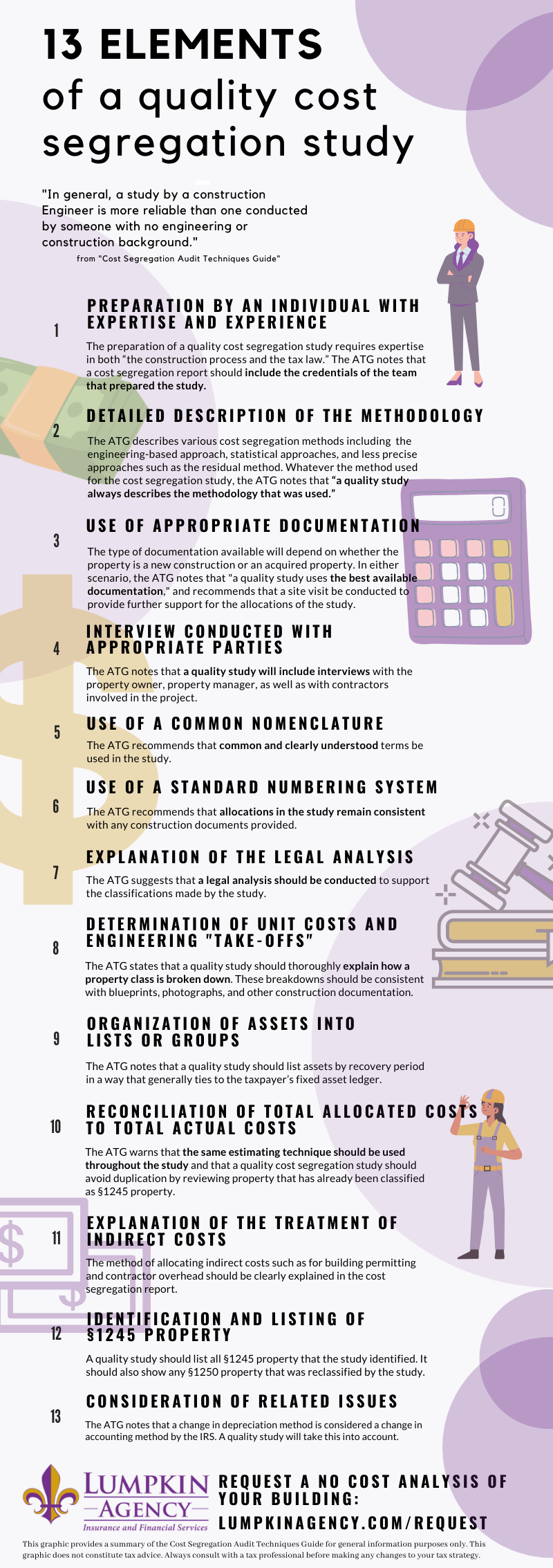

Principal Elements of a Quality Cost Segregation Study and Report [Infographic]

One crucial element of the Audit Techniques Guide is Chapter 4: Principal Elements of a Quality Cost Segregation Study and Report. This chapter of the guide provides the 13 elements of a ‘quality’ cost segregation study. According to the ATG, “quality studies greatly expedite the Service’s review, thereby minimizing the audit burden on all parties.” We’ve prepared an infographic that gives an overview of the 13 elements.

Conclusion: Consult with a Qualified Cost Segregation Professional

Cost segregation studies are complex undertakings that require a breadth of expertise and experience. The IRS Audit Techniques Guide outlines the complexities of cost segregation studies and also lists the 13 elements that define a “quality study.”

A small or medium-sized accounting firm often does not have the bandwidth to complete a cost segregation study that aligns with the 13 elements of a quality study outlined in the ATG. Between the calculations, construction expertise, interviews, and site visits that are crucial to a quality study, it makes sense for taxpayers and their accounting team to partner with a specialized cost segregation firm that uses an engineering-based method.

Our company follows the guidelines provided by the ATG. In the unlikely event of an audit, our company provides audit support. If you are considering a cost segregation study on your property, consider working with a firm that relies on the engineering-based approach considered reliable by the Audit Techniques Guide. The next step for you is to request a no-cost analysis of your real estate for yourself or on behalf of your clients.

For more information please contact our Director of Cost Segregation at clayton@lumpkinagency.com.

The information provided in this blog is intended for general information only, and is not meant to constitute tax advice.